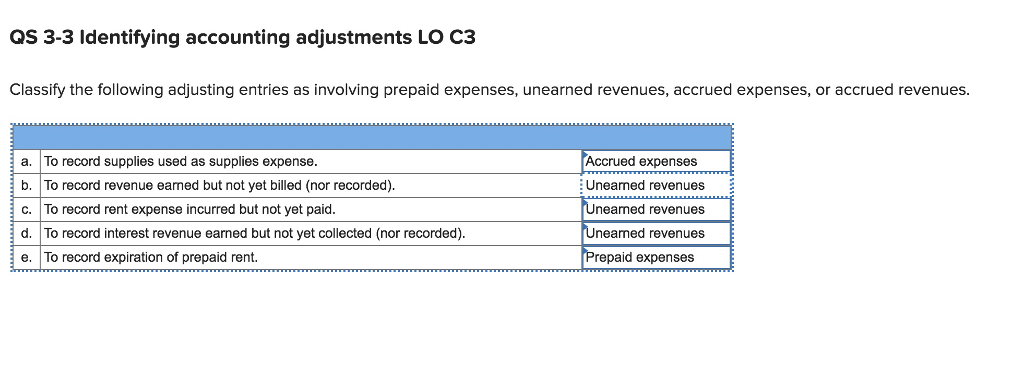

- Home loan insurance coverage for money which can be off individual institutions such as for instance finance companies is named private financial insurance coverage (PMI) and can possess a payment per month off 0.3 to one.5 % of one’s loan’s full.

- New USDA financial – that have a zero advance payment brighten and you will low interest rates – is perfect for straight down-earnings individuals who want to live rurally or in suburbs.

- People favor the latest FHA mortgage when they’re perhaps not certified into Virtual assistant mortgage, overqualified into USDA financial or maybe http://paydayloancolorado.net/west-pleasant-view just should alive somewhere perhaps not rural.

Your consumer get one part of prominent – you both you need insurance coverage into priciest contents of your existence.

You are familiar with homeowners insurance for those funded from the a normal financing, but what will be distinctions with federal home loans?

Because you are almost certainly aware, mortgage insurance getting funds which can be off personal institutions eg banking companies is named personal financial insurance rates (PMI) and can provides a payment per month of 0.step 3 to just one.5 percent of the loan’s complete.

The consumer you will avoid expenses PMI on condition that a down-payment away from 20 percent or maybe more is offered right up by the borrower. That is taxation-allowable, which is a comfort, yet still quite an amount out of change to the user.

The USDA home loan – which have a zero deposit perk and low interest rates – is perfect for down-income consumers who would like to real time rurally or perhaps in suburbs (provided the space people is actually less than ten,000).

Furthermore higher as the mortgage insurance policy is not essential. The fresh new debtor will have to pay a funding percentage, yet not. Brand new money fee is funded on financing.

Its an enthusiastic honor so you’re able to suffice those who have supported us. Whether a seasoned, productive obligations or certified surviving lover, you will want to do all you can for Virtual assistant house loan-qualified subscribers.

Just as the USDA financial, the fresh new Virtual assistant financial need zero advance payment or private financial insurance. This may lay military household relaxed if it’s its time for you to purchase property.

Consumers like new FHA home loan while they are perhaps not licensed with the Virtual assistant home loan otherwise was overqualified to your USDA mortgage (or just need certainly to live somewhere perhaps not rural).

FHA is a wonderful option for those rather than a hefty off fee. FHA is even of good use once the interest levels of these funds are usually lower than antique mortgages.

FHA terms of mortgage insurance rates differ commonly on the prior solutions, yet, if your visitors is placing over 20% having a deposit, it doesn’t affect them.

FHA lenders need a-one-date, upfront financial top (MIP) commission. Better yet, FHA fund require extra monthly MIP repayments adding up into the annual MIP.

The newest initial MIP is just one-day percentage in fact it is always step one.75 per cent of the house loan’s worthy of. The actual only real big date it will not be is if the newest FHA financial are sleek before .

The level of the fresh new income tax-deductible annual MIP away from FHA times dated , ranged from one.3 to one.55 percent to possess loans having terminology more a beneficial 15-12 months installment several months.

Amanda Rosenblatt try a writer for Federal Financial Stores, in addition to Virtual assistant Financial Locations

That it, without a doubt, was pending into level of the loan. Financing which have words lower than fifteen years with wide variety below or more than $625,000 during this time was basically 0.45 in order to 0.7 %.

Creating on , yearly MIP standards getting finance more than a fifteen-seasons title changed to your finest. The new commission prices dropped from.step 3 to just one.5 % down seriously to 0.8 to just one.05 percent.

To place toward angle – a great $3 hundred,000 loan that have a thirty-seasons name back into 2013 do pricing $step 3,900 to possess yearly MIP. Today, it might be doing $2,550.

Stretched loan repay conditions mean quicker attention to people; this is very guaranteeing as the insurance policies will cost them smaller, also.